Alberto Pototschnig - "The Internal Market - 25 years on"

Expert Articles

Part-time professor and Deputy Director (World of Practice), Florence School of Regulation and Director, DFC-Economics

The Internal Energy Market: 25 years on

by Alberto Pototschnig

In the energy sector, the European Union has been working since the early 1990s to create an Internal Market for electricity and gas, in which the vertically-integrated energy companies operating at that time in many countries would be unbundled, competition would be introduced in the wholesale and retail segments, consumers would be able to choose their energy suppliers and electricity and gas would move seamlessly between Member States. This process was expected to benefit energy consumers in terms of more choice and ‘better’ prices [1] and was supported by a sequence of legislative packages. It took new impetus after an Inquiry by the European Commission in the mid-2000s found that there were still significant barriers to the development of a fully competitive Internal Energy Market (IEM) [2], including too much concentration in most national energy markets and the lack of transparently available market information leading to distrust in the pricing mechanisms.

With the 2009 Third Energy Package, rules for cross-border exchanges of electricity and gas were reinforced, supported by a stronger governance framework with the establishment of the Agency for the Cooperation of Energy Regulators (ACER) and the European Networks of Transmission System Operators for gas and electricity (ENTSO-E and ENTSOG). This framework also provided for Network Codes and Guidelines to be developed, to define the implementation rules for the harmonisation and integration of electricity and gas markets across the Union.

For the electricity sector, the target model (ETM) had already been developed during the 2000s, structured in five pillars, covering respectively capacity calculation, the forward market, the day-ahead market, the intraday market, and the balancing market. A different target model for the gas sector was developed in 2011 and revised in 2015, focusing on metrics on the market participants’ needs and the health of the market [3].

The ETM was enshrined into legislation by the Third Energy Package and more specifically in the Network Codes and Guidelines provided for therein. A central pillar of the ETM was, and still is, the price-based coupling of the day-ahead markets across the EU to ensure that the transmission capacity between the different market zones is used to its highest value, i.e. to flow electricity from where it is cheaper to generate to where it is most valuable.

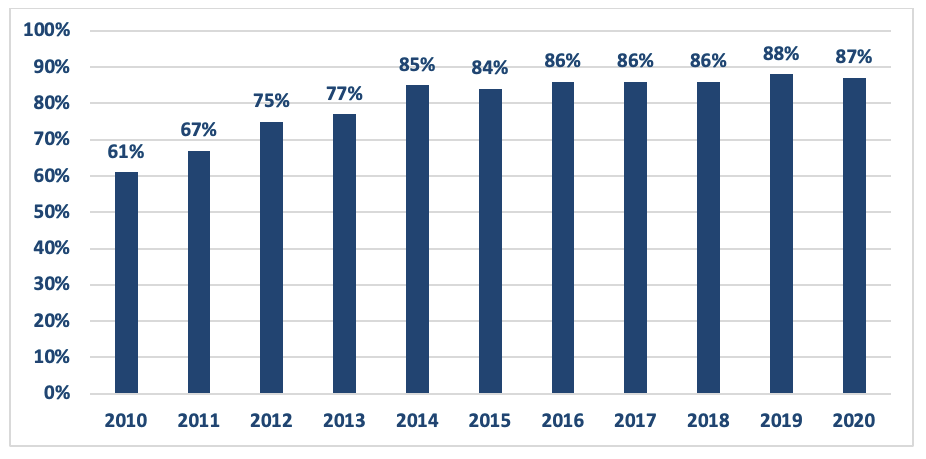

The following chart shows the degree of efficiency in the use of the cross-zonal capacity in the IEM during the period between 2010 and 2020, i.e. before the COVID pandemic and the ensuing energy crisis greatly impacting the electricity market, an aspect to which I will return later.

Chart 1 – Efficiency in the use of the electricity cross-zonal capacity in the European Union

The chart shows that the degree to which cross-zonal interconnection capacity was used to flow electricity in the right economic direction increased from just over 60% in 2010 to close to 90% in 2020. It is also noticeable that most of the progress was achieved in the period before 2015, when the Network Code on Capacity Calculation and Congestion Management, containing the rules governing the day-ahead market coupling, was adopted. This was the result of the voluntary early implementation of the ETM promoted by the Electricity Regional Initiative established by European Regulatory Group for Electricity and Gas (ERGEG) in the mid-2000s and to which stakeholders from all constituencies of the electricity sector contributed.

The increase in the efficiency in the use of the cross-zonal interconnection capacity is deemed to have resulted in net benefits for European electricity consumers in the order of one billion euro per year. Benefits to final consumers is, in fact, the crucial test for any energy sector reform.

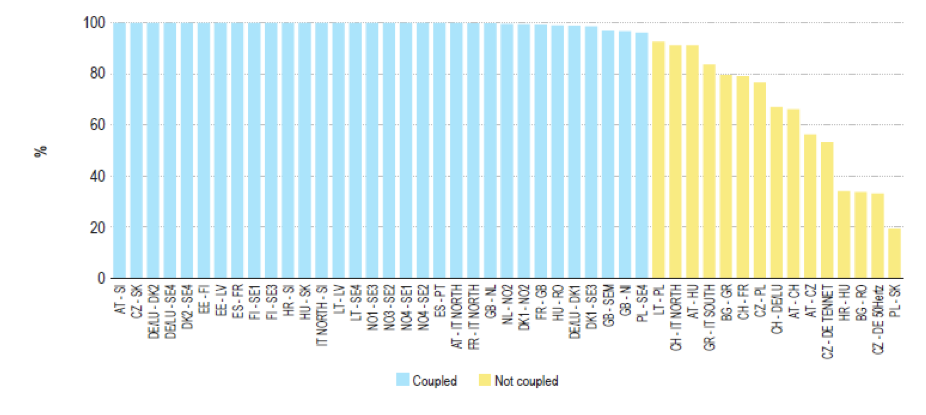

The role of market coupling in ensuring that electricity flows in the right economic direction is made even clearer by the following chart, which, with reference to the year 2020, shows that cross-zonal borders on which market coupling was implemented achieved full efficiency in the use of the interconnection capacity, while electricity was still flowing some of the times in the wrong direction where market coupling was not yet in place.

Chart 2 – Efficiency in the use of the electricity cross-zonal capacity in the European Union in 2020

In this sense it is fair to say that the EU Internal Electricity Market has been the most successful electricity market integration project ever undertaken worldwide and it is today the largest electricity market in the world and, for the most part, one that is functioning very well and delivering tangible benefits to consumers.

Such benefits became even more apparent in more recent years, where the Internal Electricity Market helped the European Union manage a number of challenges, such as the problems encountered by the nuclear-based generating fleet in Belgium and France and the energy crisis due, initially, to the faster-than-expected recovery of energy demand after the COVID pandemic and, later on, to the impact on the energy market of the unjustified and unprovoked invasion of Ukraine by the Russian Federation army. In all these cases, the IEM helped flow electricity and gas to where it had the greatest value, contributing to avoid supply interruptions. In all these cases, the ‘invisible hand’ of a well-functioning market achieved what no political negotiations between EU Member States could have probably achieved, and for sure in a much shorter time.

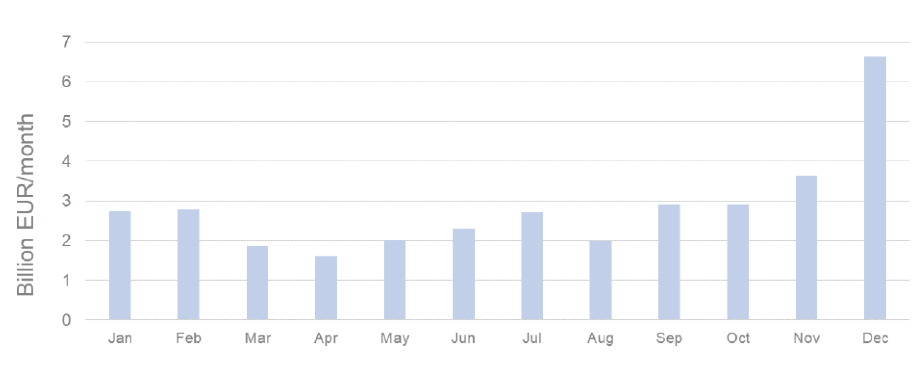

The following chart shows the estimated monthly welfare benefits provided by the Internal Electricity Market during 2021, in excess of 30 billion euro over the year, at the time when electricity prices started to rise, fuelled by increasing gas prices. The welfare benefits in this chart are evaluated with respect to a counterfactual without any interconnection capacity.

Chart 3 - Estimated monthly welfare benefits from cross-border electricity trade in 2021

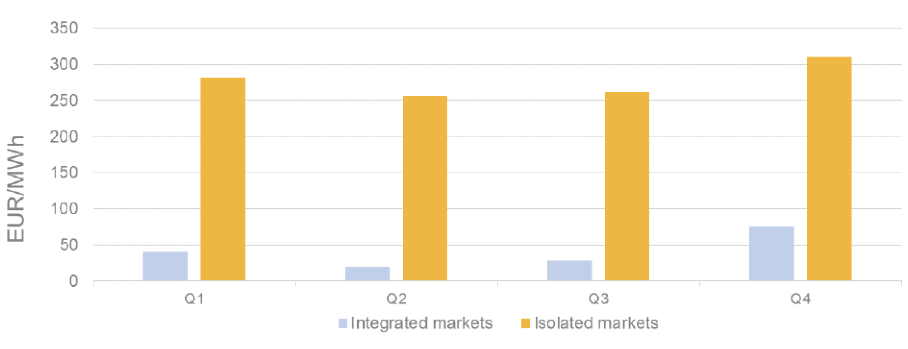

During the same period, and more recently, the Internal Electricity Market helped dampen the volatility of electricity prices in the EU. The following chart compares the observed price volatility in 2021 with the volatility of electricity prices which would have emerged without cross-border exchanges. It shows clearly that in this latter case, the volatility would have been seven times higher than what we experienced.

Chart 4 - Price volatility (EUR/MWh) in integrated and isolated electricity markets in the EU in 2021

The increase in energy prices, which started in the second half of 2021, prompted a debate on the electricity market design. A number of Member States proposed changes to such a design. Some of these proposals were interpreted as calling for replacing the current ‘pay-as-cleared’ pricing mechanism in the day-ahead market with the ‘pay-as-bid’ approach. The narrative accompanying such calls questioned why resources offering electricity in the market should receive a price which is higher than the one they are happy to accept. This narrative is very appealing from a communication viewpoint and may well lure some politicians and commentators. In fact, this is a debate which re-emerges every ten years or so, and it has been solved already many times. The fallacy of the argument supporting the call to switch to the ‘pay-as-bid’ pricing mechanism is that it assumes that market participants maintain their bidding strategy unchanged, irrespective of the market pricing mechanism. This is clearly an untenable assumption, and, in fact, the ‘pay-as-bid’ pricing mechanism would hardly deliver significant reductions in the payments to electricity producers, but likely result in a less efficient market outcome and discourage the participation in the wholesale market of smaller players, thus potentially reducing competition. It should be welcomed with a sigh of relief that the recent electricity market design reform, while enhancing the forward market, has left the pricing mechanism in the day-ahead market unchanged.

Another aspect of the current market design which has been the focus of much debate is its geographical structure. The EU, in contrast with the US which mainly opted for a nodal configuration, has chosen a geographical structure based on price zones. These price zones have widely different dimensions, from the larger ones, covering entire large Member States – such as in the case France, Poland, Spain and Germany (the latter sharing its price zone with Luxemburg), to the smaller ones, covering small Member States – such as the Baltic Member States – or only parts of Member States – as in the case of Denmark, Italy and Sweden. The current price zone configuration is, in fact, the result of a combination of historical arrangements, electricity network topology and political considerations. Legislation calls for this configuration to be periodically reassessed on the basis of its “ability to create a reliable market environment, including for flexible generation and load capacity, which is crucial to avoiding grid bottlenecks, balancing electricity demand and supply, securing the long-term security of investments in network infrastructure” [1]. It envisages a structured bidding zone-review process where alternative configurations are considered and compared with respect to a number of criteria. A first informal bidding zone review was carried out in 2018 and did not deliver any conclusive result. The first formal review was launched in 2019 and it is still ongoing. Unfortunately, legislation [2] provides a long list of criteria – thirteen, grouped in three categories - to be considered, probably too many to make any alternative configuration standing out as a better one with respect to the current setting. In particular, one criterion seems particularly insidious, as it might be easily misinterpreted; it refers to “market liquidity, market concentration and market power.” This criterion has so far been used to support larger bidding zones which, prima facie, promote market liquidity and competition. However, this is the case only if these zones are supported by a network which do not constrain intra-zonal exchanges. If, instead, frequent congestion occurs within these large bidding zones, which cannot be managed in the market [3], such a liquidity is only apparent, and so is the greater competition among market participants that larger zones are credited with promoting. In real time, the network limitations will emerge and remedial actions – such as redispatching - will have to be performed, revealing the inconsistency of the bidding zone configuration with the network topology. Any intra-zonal exchanges which violate the physical limit of the network would have to be redispatched and market participants on different sides of congested network elements within the same zone would find themselves not really competing against each other. In recent years, re-dispatching costs in the EU have spiralled up and they are largely due to network congestion at transmission level [4]. In Germany, remedial action costs increased from 1.3 bn€ in 2020 to 2.8 bn€ in 2022, or almost 6€ per MWh consumed by German consumers, and 87% of such costs related to redispatching.

It is to be hoped that the current review process delivers a bidding zone configuration which is well aligned with the capabilities of the network, so that most of the congestion can be managed in the market, rather than after the market. This is probably the last major unresolved issue of the progress in the electricity market integration so far, before we embark in implementing the enhancements, e.g. in the design of the long-term market, introduced with the electricity market design reform just adopted by the co-legislators.